Using a Cosigner on USDA Loan Apps

Understanding

the Rule

Understanding

the Rule

The U.S. Department of Agriculture (USDA) Rural Development Guaranteed Loan Program prohibits non-occupant cosigners on all single-family housing loans. This restriction, outlined in the agency's technical handbook, is a fundamental eligibility requirement that separates USDA loans from many conventional and FHA loan programs.

According to USDA Handbook 1-3555, Chapter 9, Section 2, "Repayment income will determine if the applicant(s) has sufficient income to repay the mortgage in addition to recurring debts." Critically, "Cosigners and non-occupant co-borrowers are not permitted for a guaranteed loan transaction" (7 CFR 3555.152(a)).

Why This Rule Exists

The prohibition on non-occupant cosigners reflects the USDA program's core mission: assisting low- to moderate-income borrowers in rural areas who lack sufficient resources to qualify for traditional conventional financing. By requiring all parties to the note to be owner-occupants and contributors to household income, USDA ensures that repayment capacity is genuinely sustainable and that loans are structured for borrower strength rather than external guarantees.

The focus is on documented, stable, and dependable income from parties who have a direct financial stake in the property. This approach reduces default risk and aligns with USDA's underwriting philosophy, which emphasizes genuine repayment ability.

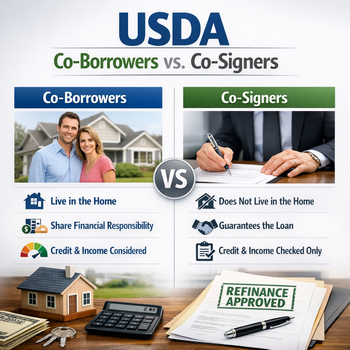

Co-Borrowers vs. Cosigners: The Critical Distinction

Borrowers often confuse cosigners with co-borrowers, but USDA treats them very differently:

Non-Occupant Cosigners (Not Permitted): A cosigner is a person who guarantees the debt but does not occupy the property and whose income is not counted toward repayment qualification. They are simply signing to back the borrower's obligation. USDA does not allow this arrangement.

Occupant Co-Borrowers (Permitted): A co-borrower is a person who will occupy the property as their primary residence, is a party to the promissory note, and whose income qualifies toward the debt-to-income (DTI) ratio. USDA permits co-borrowers if they meet all standard credit and income requirements.

Documentation and Verification Requirements

When co-borrowers are included on a USDA loan, their income must meet the same stability and documentation standards as the primary borrower. USDA requires:

- Federal income tax returns or IRS tax transcripts with all schedules

- Written verification of employment (VOE) or electronic verification

- Evidence of stable, dependable earnings

- Analysis of employment gaps

- Documentation that the co-borrower will occupy the property as their primary residence

These requirements ensure that co-borrower income is legitimate, verifiable, and sustainable for the loan's duration.

Program Consistency

This restriction is consistently applied across all USDA Guaranteed Loan Program products, including purchase transactions, refinances, and construction loans. The USDA's Frequently Asked Questions document explicitly confirms: "No, cosigners and non-occupant co-borrowers are not permitted."

What Borrowers Should Know

If a borrower needs additional income to qualify, the solution is finding a qualified occupant co-borrower - not a cosigner. This means the additional person must:

- Be willing to occupy the property as their primary residence

- Have acceptable credit and income

- Be a party to the loan documents

- Have their income underwritten using the same standards

Conclusion

The USDA's prohibition on non-occupant cosigners is clear and without exception. This policy protects both borrowers and the program by ensuring loans are based on sustainable household income from owner-occupants. Borrowers considering a USDA loan should work with their lender to identify qualified occupant co-borrowers if additional income is needed to meet debt-to-income ratios.

References

- 7 CFR 3555.152(a) – Code of Federal Regulations, Rural Housing Service

- HB-1-3555, Chapter 9, Section 2 – USDA Handbook 1-3555: Single Family Housing Guaranteed Loan Program Technical Handbook

- HB-1-3555 Repayment Income Guidance – USDA Rural Development, Single Family Housing Guaranteed Loan Program, Repayment Income Notes

- USDA RD Single Family Housing FAQ – Frequently Asked Questions, Loan Origination, USDA Rural Development

- RD Form 3555-21 – Worksheet for Documenting Eligible Household and Repayment Income, USDA Rural Development

Connect With Us

Please share – it really helps