Comparing USDA Loans to FHA & Conventional Loans

Understand

how USDA loans stack up against other popular mortgage programs.

Compare eligibility requirements, down payments, rates, and features

to determine which loan is right for your situation.

Understand

how USDA loans stack up against other popular mortgage programs.

Compare eligibility requirements, down payments, rates, and features

to determine which loan is right for your situation.

Overview: Four Major Loan Programs

Borrowers have several paths to homeownership, each with distinct advantages and requirements. USDA loans, FHA loans, conventional mortgages, and VA loans serve different borrower profiles and financial situations. Understanding the key differences helps you choose the program that fits your needs, income level, and location goals.

USDA loans stand out for rural and suburban homebuyers with moderate to lower incomes. FHA loans serve borrowers with limited down payment funds or lower credit scores. Conventional loans are ideal for borrowers with strong credit and larger down payments. VA loans are exclusive to eligible military veterans and active-duty service members and offer unparalleled benefits with no down payment required.

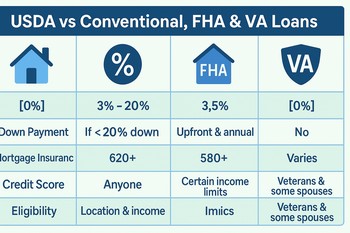

Side-by-Side Comparison Table

| Feature | USDA | FHA | Conventional | VA |

|---|---|---|---|---|

| Down Payment | 0% (100% financing) | 3.5% minimum | 3% - 20% (varies) | 0% (100% financing) |

| Credit Score Requirement | 580 (some lenders 640+) | 580 (some lenders require 620+) | 620 (best rates 740+) | No official minimum (580+ typical) |

| Debt-to-Income Ratio | 41% (up to 50% with compensating factors) | 43% (up to 50% with compensating factors) | 43% (36% preferred) | 41% (residual income method) |

| Mortgage Insurance | Guarantee fee upfront; annual fee | Upfront MIP + annual MIP (varies by LTV) | PMI if down payment < 20% | Funding fee (1.25% - 3.3%); no annual fee |

| Interest Rates | Market-based (generally competitive) | Market-based (slightly higher) | Market-based (typically lowest) | Market-based (often best rates) |

| Property Location | Rural and some suburban areas only | Any location (urban, suburban, rural) | Any location | Any location |

| Income Limits | Area-based (varies by county) | No income limits | No income limits | No income limits |

| Property Type | Primary residence only (single-family, manufactured homes, condos) | Primary residence (single-family, condos, multi-unit with FHA approval) | Primary, second home, investment property | Primary residence only |

| Refinancing Options | Streamline refinance available | Streamline refinance available | Rate-and-term and cash-out | Streamline, cash-out, and IRRRL |

| Seller Concessions | Up to 6% of the sales price | Up to 6% of the sales price | 2% - 4%, depending on down payment | Up to 4% of the sales price |

| Closing Cost Limits | Lender origination fees capped; varies by state | No regulatory caps | No regulatory caps | No regulatory caps (VA validates) |

| Loan Limits | $766,550 (2024; varies by area) | $486,000 (2024; higher in high-cost areas) | Conforming: $766,550 (2024); jumbo loans are higher | No official limit (based on county and borrower entitlement) |

| Eligibility | U.S. citizens or legal residents; income requirements | U.S. citizens or legal residents | U.S. citizens or legal residents | Eligible military members, veterans, and surviving spouses |

Detailed Program Breakdown

USDA Loans: Rural and Suburban Focus

USDA loans are designed to promote homeownership in rural America and qualifying suburban areas. The USDA Guaranteed Rural Housing Loan Program, administered by the USDA Rural Development office, targets low- to moderate-income borrowers who want to buy in specific geographic regions.

Key Strengths

- Zero down payment requirement

- No mortgage insurance (replaced with a guarantee fee)

- Favorable debt-to-income flexibility

- Lower interest rates than the FHA

- Flexible credit requirements

- Seller-paid closing costs up to 6%

Key Limitations

- Property must be in an eligible rural area (the biggest restriction)

- Income limits apply by county, preventing higher-earning borrowers from qualifying

- Loan is restricted to primary residences

- Processing times may be longer than those for conventional loans due to property eligibility verification.

FHA Loans: Accessible to First-Time Buyers

FHA loans, insured by the Federal Housing Administration, were created to make homeownership achievable for borrowers with limited savings and moderate credit. FHA loans allow down payments as low as 3.5% and accept credit scores in the 580 range, making them popular with first-time homebuyers.

Key Strengths

- Low down payment

- Flexible credit score requirements

- Available in any location

- Seller concessions up to 6%

- Streamline refinance options that require minimal documentation

Key Limitations

- Mortgage insurance is mandatory for the life of the loan if the down payment is less than 10% (11+ year commitment)

- Annual mortgage insurance premiums add to your monthly payment

- Interest rates tend to run slightly higher than conventional loans

- FHA has strict property condition and appraisal requirements

Conventional Loans: The Traditional Standard

Conventional loans are mortgages not backed by any government agency. They are sold to investors in the secondary mortgage market and follow guidelines set by Fannie Mae and Freddie Mac. Conventional loans are the most common mortgage type in the United States.

Key Strengths

- Typically, the lowest interest rates (especially with strong credit and a down payment)

- Ability to remove PMI once you reach 20% equity

- Available for investment properties and second homes

- Flexibility in loan terms

- No government restrictions on property location or borrower income

Key Limitations

- Higher down payment requirement (3% minimum, but 20% needed to avoid PMI)

- Better credit scores (620+, preferably 740+) are expected

- PMI must be paid if the down payment is less than 20%

- Debt-to-income limits are stricter than those of the FHA or USDA (43% maximum)

VA Loans: Exclusive Military Benefit

The Department of Veterans Affairs guarantees VA loans and is one of the most powerful homeownership programs available. Eligibility requires military service (active duty, reserve, or National Guard) or surviving spouse status. VA loans offer benefits that are difficult to match in any other program.

Key Strengths

- Zero down payment

- No mortgage insurance (funding fee replaces it, and is often paid by the seller)

- Typically, the lowest interest rates are available

- No prepayment penalties

- Ability to reuse your benefit

- Residual income calculations instead of strict debt-to-income ratios, allowing for higher borrowing power in some cases

Key Limitations

- Eligibility is restricted to qualified veterans, active-duty service members, and surviving spouses

- A Certificate of Eligibility (COE) must be obtained

- Funding fee (1.25% to 3.3% of the loan amount) applies unless you have a VA disability rating

- VA loans can take longer to process due to government validation requirements

Which Loan Should You Choose?

Choose USDA If:

- Your income is at or below county limits

- The property is located in an eligible rural or suburban area

- You want a zero down payment without lifetime mortgage insurance

- Your credit score is 580 or higher

- You are a first-time or repeat homebuyer

Choose FHA If:

- You have limited funds for a down payment (3.5% minimum)

- Your credit score is 580 or higher

- You want to buy in any location (urban, suburban, or rural)

- You are a first-time homebuyer

- You prefer a familiar, well-established program

Choose Conventional If:

- You have strong credit (740+ for best rates)

- You can afford a 5-20% down payment

- You want to avoid government-backed loan restrictions

- You plan to buy an investment or a second property

- You want the lowest possible interest rates

Choose VA If:

- You are an eligible veteran or active-duty service member

- You want zero down payment and no mortgage insurance

- You want access to the best interest rates

- You plan to stay in the home long-term

- You value the additional VA protections and benefits

Key Takeaway

USDA loans offer an unbeatable combination of zero down payment and no lifetime mortgage insurance for rural homebuyers within income limits. FHA loans are ideal for credit-challenged first-time buyers in any location. Conventional loans reward strong borrowers with the lowest rates and maximum flexibility. VA loans are unmatched for eligible veterans, offering the best terms and no down payment.

Frequently Asked Questions

Can I use both USDA and VA benefits at the same time?

No. You must choose one program. If you qualify for both, a VA loan typically offers better terms (no funding fee if disabled, lower rates, residual income flexibility). Consult with a lender to compare which program gives you the best overall benefit for your specific situation.

Which program has the fastest closing timeline?

Conventional loans generally close fastest (21-30 days) because they don't require government verification. USDA loans often take 45-60 days due to property eligibility verification. FHA and VA loans typically fall within the 30-45-day range, depending on the lender.

What happens if I refinance from one program to another?

You can refinance from any loan type to any other program. For example, you could start with an FHA loan and refinance to a conventional loan once your equity reaches 20% and your credit improves. USDA, FHA, and VA borrowers can also use streamline refinances within their programs for lower costs and faster approval.

Do I have to live in the home to qualify for these loans?

Yes. USDA, FHA, and VA loans all require the property to be your primary residence. Conventional loans are the only option if you want to buy an investment property or second home.

Can sellers pay closing costs with all four programs?

Yes, but limits vary. USDA and FHA allow up to 6% seller concessions. VA allows up to 4%. Conventional allows 2-4%, depending on down payment size. Seller concessions can be used to cover closing costs, prepaid items, points, or even a down payment contribution.

Which program is best for low credit scores?

All four programs accept credit scores in the 580 range, so credit alone doesn't rule you out. However, some lenders are stricter than others. USDA and FHA lenders tend to be more flexible with credit challenges if other compensating factors are strong (stable employment, good payment history, manageable debt).

Connect With Us

Please share – it really helps