USDA Property Condition and Inspection Rules

The

USDA represents a unique opportunity for low- to moderate-income

individuals to buy a home in eligible rural and suburban areas.

These mortgage loans help home buyers achieve homeownership as part

of rural development efforts. This government loan is designed to

assist those who do not qualify for conventional loans. However,

many applicants are concerned about the possibility of being denied

and the factors that could lead to that denial.

The

USDA represents a unique opportunity for low- to moderate-income

individuals to buy a home in eligible rural and suburban areas.

These mortgage loans help home buyers achieve homeownership as part

of rural development efforts. This government loan is designed to

assist those who do not qualify for conventional loans. However,

many applicants are concerned about the possibility of being denied

and the factors that could lead to that denial.

Understanding the USDA Rural Development loan program's requirements, how it works, and why a denial might occur can help applicants confidently navigate the process. It also provides a clear checklist of steps you can take to improve your chances of approval. Every home buyer's situation is different, and understanding how USDA works, including home inspection requirements, appraisals, and income qualifications, is critical for success. With USDA and FHA loans continually evolving, staying informed about current guidelines is crucial.

Understanding Credit Score Requirements

Minimum Credit Score

One of the most critical factors in securing a USDA is meeting the minimum credit score requirements. For most government loan programs, including USDA and FHA loans, a minimum credit score of 620 is required, though a score of 640 or higher is preferred. A higher score can improve your chances of getting approved and result in a lower interest rate.

Mortgage lending professionals use your credit score to evaluate your history of managing debt and making timely payments. A higher score shows you're less risky. VA and USDA often follow similar guidelines in this regard. The appraiser may also consider your financial stability during the loan approval process.

Impact of Credit Report

Your credit report plays a significant role in the loan approval process. Negative marks like late payments, accounts in collections, or a history of bankruptcy can hurt your chances. If there are any issues in your credit history, it's essential to address them before applying for a USDA loan. A USDA home inspection may also reveal problems that could impact approval, which is why preparation is critical.

Tips for Improving Your Credit Score

- Pay down outstanding debts: Reducing credit card balances or paying off loans can improve your credit utilization ratio.

- Correct errors on your credit report: Mistakes on your credit report can negatively affect your score, so check your report carefully and get mistakes corrected.

- Make payments on time: Timely payments on loans and credit cards are one of the best ways to boost your credit score over time and help you qualify for government loan programs.

Addressing credit issues early on can significantly improve your chances of success when applying for a USDA loan.

Income and Debt Considerations

Evaluating Income and Debt

Lenders will evaluate your gross monthly income and debt obligations to determine whether you can afford the loan. This helps them calculate your debt-to-income (DTI) ratio, which compares how much you owe each month to how much you earn. The lower your DTI, the better your chances of being approved. USDA buyers must meet specific income requirements to qualify.

The location of the home you want to buy also plays a significant role. For the loan to proceed, the property must be located in a rural or USDA-eligible suburban area.

Income Limits and Ratios

USDA rural development loans have income limits that vary by region. These limits are based on the median income in the area where the property is located. For a home to qualify for USDA financing, your household income must not exceed 115% of the area's median income. However, applicants must also show they can afford the mortgage by meeting minimum income requirements.

Steps to Qualify

- Ensure your household income falls within USDA guidelines for your area.

- Provide proof of income, including pay stubs, tax returns, and relevant financial documentation.

- Calculate your DTI ratio to ensure it's within acceptable limits, typically above 41%.

Property Requirements and Valuation

Property Location

The location of the home you're buying is one of the most critical factors in qualifying for a USDA loan. Homes must be located in rural areas or specific suburban zones to qualify for USDA financing. If the house is located outside these eligible areas, it cannot qualify for a USDA loan. This is part of the government's focus on rural development.

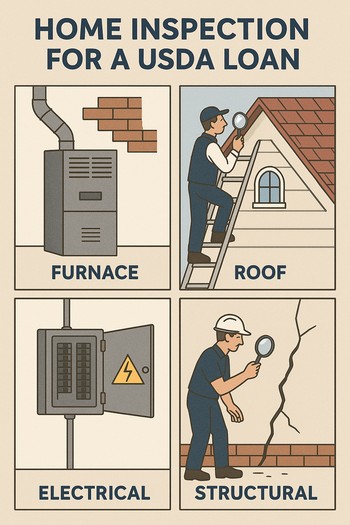

Appraisal and Condition

The property must meet USDA's standards, and a USDA appraisal is required to ensure the home's value aligns with the loan amount. This appraisal checklist ensures the house is safe, structurally sound, and meets HUD health and safety standards. Additionally, an inspection report is needed to verify the home's condition. A home inspection checklist typically includes checking for termite damage, structural integrity, and compliance with USDA appraisal guidelines.

Key Property Requirements

- The property must be your primary residence (no second homes or investment properties).

- The home must meet USDA health, safety, and structural standards.

- The appraised value of the home must match or exceed the purchase price.

The loan may be denied if the home fails to meet these requirements. However, minor repairs or adjustments can often bring the property into compliance.

Working with Financial Professionals

Role of a Loan Officer

Navigating the USDA can be complicated, especially for first-time home buyers. Working with a knowledgeable loan officer can help you understand the eligibility requirements and guide you through the application process. These professionals can assist with the necessary paperwork and help you gather the documentation needed for a smooth loan closing. The loan officer also coordinates with the home inspector and appraiser to ensure the home meets USDA standards.

Approved Lenders

Not all lenders are approved to offer USDA loans, so working with a USDA-approved lender is essential. These lenders understand the intricacies of USDA rural development loans and will help ensure the loan process runs smoothly. They can also help you navigate the various government loan programs, including FHA and USDA, to determine the best fit for your situation.

Common Reasons for Loan Denial

Several factors can lead to a USDA loan being denied. Being aware of these potential issues can help you address them before applying.

Common Reasons for Denial

- A credit score below 640: Most lenders prefer applicants with a credit score of 640 or higher.

- High debt-to-income ratio: Lenders may view you as a higher risk if your debt takes up too much of your monthly income.

- The home does not meet USDA eligibility standards: Homes that don't meet USDA inspection requirements, location guidelines, or property value standards will not qualify.

- Income verification issues: Failing to provide accurate income documentation or failing to meet income requirements can result in denial.

- Employment history concerns: Lenders prefer applicants with stable, long-term employment to reduce the risk of loan default.

Time Factors in Loan Approval

The time it takes to get approved for a USDA loan can vary based on several factors, including the completeness of your application and the efficiency of your lender. The workload of both the lender and the appraiser, along with any issues revealed in the inspection report, can also affect USDA loan approval.

Factors Affecting Loan Approval Time

- The lender's and appraiser's workload.

- The completeness of the application and documentation.

- The availability of required documents from the buyer, seller, and appraiser.

- The timing of the USDA home inspection, appraisal, and other steps.

Being well-prepared and working with a proactive loan officer and appraiser can help streamline the approval process.

Steps to Improve Approval Chances

If you're concerned about being denied, there are several steps you can take to improve your chances of getting approved for a USDA loan.

Key Steps to Improve Approval

- Aim for a credit score of 680 or higher to increase your approval chances and secure better interest rates.

- Pay off debts to lower your DTI ratio, making you a more attractive borrower.

- Maintain stable employment, as this reassures lenders that you have the stability to repay the loan.

- Ensure the property meets USDA eligibility standards, including location and structural requirements.

- Prepare all necessary documentation, including pay stubs, tax returns, and bank statements, in advance.

Understanding USDA Lenders

Application Process

The USDA loan application process requires specific documentation to verify income, employment, assets, and the property's eligibility.

Typical Documentation Required

- Income verification (pay stubs, tax returns, W-2s).

- Bank statements to show proof of assets.

- Employment history documentation.

- Debt obligations (credit card statements, loan balances).

- Property eligibility documents, including the appraisal and home inspection report.

Being organized and prepared with all required paperwork can help expedite the loan finalization process.

Alternative Options if Denied

If your USDA loan is denied, you can explore other mortgage programs to buy a home. VAs, FHA loans, and conventional loans can provide alternative pathways to homeownership.

Alternative Loan Options

- FHA loans: These government-backed loans have lower credit score requirements and down payment options, though they come with mortgage insurance premiums.

- VA s: If you're a veteran, a VA loan may be an excellent option, as VA appraisal rules are typically more lenient, and no down payment is required.

- Conventional loans: Traditional loans might be an option if you meet the credit and income requirements.

- State-specific programs: Many states offer home buyer assistance programs to help with down payments or closing costs.

- Down payment assistance programs: Some government and nonprofit programs offer grants or loans to help cover the down payment on a home.

Regional Considerations

Geographic Eligibility

USDA loans are designed to promote homeownership in rural areas, though some suburban regions also qualify. Confirming that the property address you're interested in is in an eligible area before applying for a USDA loan is essential.

Population Growth Impact

As areas grow and become more urbanized, they may lose their USDA eligibility. If you're considering buying a home near an urban area, verifying the property's eligibility status is crucial to avoid complications during the loan process.

Financial Preparation

Critical Financial Considerations

Review your financial situation before applying for a USDA loan. This will ensure that you are prepared for the financial responsibilities of owning a home.

Important Financial Steps

- Review your credit report and correct any errors that could lower your score.

- Calculate your gross monthly income to confirm you meet the loan's income requirements.

- Assess your monthly debt obligations to ensure they're manageable.

- Determine the maximum loan amount you qualify for to focus on affordable properties.

- Understand the total cost of homeownership, including taxes, insurance, and maintenance.

Impact of Market Conditions

Current market conditions can impact the USDA loan process. Rising home prices, fluctuating interest rates, and increased competition can all affect your ability to secure a loan.

Factors Affected by Market Conditions

- Property valuations: Changes in the home's appraised value can affect your loan.

- Interest rates: Higher interest rates can increase your monthly mortgage payment, making the home less affordable.

- Processing times: During periods of high demand, loan approval times may take longer due to the high volume of applications.

- Limited inventory in eligible areas: As rural areas develop, finding a USDA-eligible home can become more challenging.

Documentation Requirements

You must provide various documents to complete your USDA loan application. Having these prepared ahead of time can help ensure the process runs smoothly.

Required Documents

- Income verification, such as pay stubs and tax returns.

- Recent bank statements to show proof of savings.

- Employment verification letters or calls to confirm employment history.

- Debt obligations, including loan and credit card balances.

- Appraisal and home inspection reports to ensure the property meets USDA standards.

Future Considerations

Post-Approval Factors

Even after securing a USDA loan, several ongoing responsibilities are required to maintain homeownership.

Key Post-Approval Responsibilities

- Maintaining the home: Ensure that the home remains in good repair, as its condition must meet USDA standards throughout the life of the loan.

- Staying current on insurance and taxes: Homeowners must pay property taxes and insurance premiums to avoid default on their loans.

- Monitoring property value: Track your home's value to understand its appreciation over time.

Building Long-Term Success

Success with a USDA loan doesn't end once you're approved. Maintaining healthy financial habits and staying informed about program changes can help you build long-term economic success.

Long-Term Financial Tips

- Maintain a good payment history: Timely mortgage payments help maintain your credit and build home equity.

- Avoid taking on too much additional debt after closing on the home.

- Monitor your credit report regularly to catch any issues early.

- Stay informed about changes to USDA or FHA loan guidelines to remain eligible for refinancing if needed.

- Consider refinancing if market conditions improve to secure a lower interest rate.

Final Thoughts

While USDA loan denial is possible, understanding and preparing for the program's requirements can improve your chances of approval. By addressing credit, income, or property eligibility issues, you can be in a solid position to qualify for the loan.

Other mortgage programs, like FHA or conventional loans, are available even if your application is denied. Working with experienced professionals, maintaining sound financial habits, and staying focused on meeting USDA loan criteria can help you achieve your homeownership goal. With careful planning and persistence, you can explore all available options to find the best loan solution.

Connect With Us

Please share – it really helps