USDA Loan Well Water Testing Requirements: What You Need to Know

When you apply for a USDA loan to purchase a rural home with a private well, one critical hurdle stands between you and closing day: water testing. The United States Department of Agriculture has specific well water test requirements that your property must meet before the agency will approve your mortgage. These requirements protect you and your family by making sure your drinking water meets federal safety standards.

When you apply for a USDA loan to purchase a rural home with a private well, one critical hurdle stands between you and closing day: water testing. The United States Department of Agriculture has specific well water test requirements that your property must meet before the agency will approve your mortgage. These requirements protect you and your family by making sure your drinking water meets federal safety standards.

Understanding what the USDA expects from a water test can save you time, money, and stress. This guide walks you through every aspect of well water testing requirements, from what gets tested to where you send samples and how long results take. Whether you're a new homebuyer or returning to rural living, knowing these rules upfront keeps surprises off your closing table.

Why USDA Loans Require Well Water Testing

The USDA doesn't require water testing just to be difficult. The agency backs loans on rural properties where municipal water supply systems don't exist. That means homeowners rely entirely on private wells or cisterns for their drinking and household water. Without federal oversight, some of these water systems might harbor contaminants that cause serious health problems.

A water test documents that your well meets minimum safety standards before you sign a mortgage. The United States Environmental Protection Agency and state health authorities set these benchmarks. When you get a USDA loan, you agree to comply with them. Think of it as a health checkup for your home's water supply - just like a home inspection protects your investment in the structure itself, a water quality check protects your investment in safe, clean drinking water.

For FHA loans and VA loans, similar rules apply. Each loan program requires documentation that your water source meets federal and state drinking water standards. The USDA's approach is clear: no safe water, no loan approval.

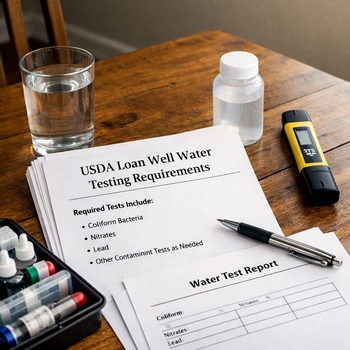

What Gets Tested: The USDA Well Water Test Requirements Checklist

Not all water samples are created equal. The USDA and your state's health department define exactly which contaminants must be checked. Understanding this list helps you know what to expect when you schedule your water test.

Bacterial testing forms the foundation of any well water test. The sample is sent to a certified laboratory to test for coliform bacteria, which indicate that your well may be contaminated by sewage or surface runoff. Total coliform results must show zero or non-detect. If your initial sample shows coliform, you'll need a follow-up water sample after the well is treated and flushed.

Chemical testing rounds out the testing requirements. Labs test for nitrate levels, which can come from fertilizers, animal waste, or septic systems. The maximum contaminant level for nitrate is 10 milligrams per liter. If levels exceed this, your well fails the water test requirements. Lead and other heavy metals are tested depending on your state's rules and well construction details.

Here's what a typical USDA loan water test covers:

- Total coliform bacteria – Must be absent (non-detect)

- Nitrate – Must be below 10 mg/L

- Lead – Results reported; levels above 15 ppb trigger action

- Arsenic – Varies by state; typically below 10 ppb

- pH level – Usually between 6.5 and 8.5

- Turbidity – Measures cloudiness; should be low

- Hardness – General mineral content (informational)

- Iron and manganese – State-dependent limits

Your state health authority may require additional tests. In Florida, for example, sulfate and radon testing might be needed. Always ask your lender which tests your specific property must pass to meet USDA loan requirements.

How to Arrange Your Well Water Test

Your lender will tell you who must perform the water test. Most lenders require that a certified laboratory approved by your state handles the work. You can't simply use a DIY kit and call it done. The United States Environmental Protection Agency and state departments oversee which labs qualify to test drinking water samples for regulatory compliance.

Here's the typical process for scheduling a well water test:

Step 1: Get your lender's approval. Before ordering any water testing, ask your loan officer which certified laboratory they accept and whether they have a preferred vendor. Some lenders maintain relationships with specific labs for faster turnaround.

Step 2: Contact the laboratory. Call or email the lab to schedule a sample collection. They'll provide sterile bottles along with specific instructions for taking your water sample. Contamination during collection ruins the results and wastes your money.

Step 3: Take the sample properly. The lab technician or your plumber will usually collect the water sample directly from your well or a cold-water tap closest to the well head. You must follow chain-of-custody procedures - essentially proving the sample stayed clean and uncontaminated from collection through delivery.

Step 4: Pay and wait. Most water testing runs $150 to $400 depending on how many contaminants get tested. Results typically arrive within 5 to 10 business days, though rush options exist for urgent closings.

Step 5: Share results with your lender. Once the certified laboratory releases test results, send them straight to your loan officer. Your lender reviews them to confirm compliance with USDA standards.

When Your Well Fails the Water Test

If your water test shows contamination, don't panic. Many problems are fixable, and your USDA loan water approval isn't automatically dead. Your next step depends on what the test results revealed.

Bacterial contamination (coliform): This is often the easiest to fix. A licensed well contractor flushes and disinfects your well, then retests. Once the follow-up water sample shows zero coliform bacteria, you're cleared. This typically costs $200 to $500.

Nitrate above limits: This is harder to resolve quickly. High nitrate suggests a persistent problem - perhaps a failing septic system nearby or agricultural runoff. Installing a treatment system (like reverse osmosis or ion exchange) can take weeks and cost $1,000 to $5,000. Some buyers negotiate with the seller to have treatment installed before closing.

Lead or arsenic: Treatment systems work, but they're expensive and require regular maintenance. Many buyers ask sellers to handle this before purchase, or they renegotiate the price to cover treatment costs.

pH or hardness issues: These are usually reported for your information but don't automatically fail a water test requirements check. High hardness might indicate the need for a water softener (optional), while an unusual pH might point to naturally occurring minerals.

Should problems persist after a second water test, your lender may deny the USDA loan or demand you to sign a waiver accepting the risk. In rare cases, the property simply won't qualify for USDA financing, and you'd need to explore FHA or conventional options - if those lenders will even approve it.

USDA Well Water Testing Requirements by State

While the USDA sets baseline standards for water quality, individual states add their own rules. Your state health authority may require additional testing beyond what the USDA demands. This is why talking to your lender and local health authority early matters so much.

Here are some variations throughout various regions:

| Testing Element | USDA Standard | State Variation |

|---|---|---|

| Coliform bacteria | Non-detect (zero) | All states require this; most states are identical |

| Nitrate | 10 mg/L maximum | All states follow federal standard |

| Lead | Reported; 15 ppb action level | Some states have stricter limits |

| Arsenic | 10 ppb maximum | Some states test more frequently |

| Additional tests | None required | Varies: radon in some areas, uranium in others |

Contact your state's local health authority or environmental protection agency to confirm exact testing requirements for your county. Various regions have unique concerns - Florida tests for radium and radon, while western states may test for uranium. The United States Environmental Protection Agency maintains a database of state-specific requirements for researching your area.

Documents You'll Need for Your USDA Loan Closing

When you're ready to close on your USDA home loan, your lender will request particular documentation proving your water test passed. Know what to gather so nothing delays your mortgage approval.

The lab report: This is the main document. It lists all contaminants tested, the results, and the name and certification number of the certified laboratory. Make sure the report is signed by the lab director or qualified technician.

Chain of custody form: This proves your water sample stayed uncontaminated from collection through testing. It should show who collected the sample, when, and who handled it afterward.

Well construction details: Some lenders want a copy of your well's construction report or a licensed plumber's assessment of well condition. This helps lenders determine whether bacterial contamination indicates a fixable problem (such as a cracked well seal) or a more profound issue.

Treatment documentation: If your well failed initially but passed after treatment, keep records of what was done. A plumber's invoice showing well disinfection or treatment system installation proves the work was completed professionally.

Variance letters (if needed): In rare cases where your results slightly exceed limits but your local health authority has approved your well, get written approval from public health officials. This letter tells your lender that despite the high reading, your well meets local standards.

Organize these documents now. Your loan officer will request them shortly before closing, and having them ready keeps your timeline on track.

Frequently Asked Questions About USDA Well Water Testing

How long does a well water test take for a USDA loan?

Most results arrive within 5 to 10 business days from the time the certified laboratory receives your water sample. Collection itself takes one visit - usually 30 minutes to an hour. If your water test initially fails and you need treatment, add 1 to 4 weeks for repairs and retesting. Some labs offer rush testing for an extra fee if you're working against a final deadline.

Can I test my own well water at home?

Home test kits exist and can give you a rough idea of your well water quality, but they don't satisfy USDA loan water test requirements. Your lender requires results from a state-certified lab that adheres to strict protocols. The only exception is if you're testing for personal knowledge before applying - in that case, home kits are fine, but don't use them as your official water test for the loan.

What happens if my well water test fails?

It depends on what failed. Bacterial contamination is usually resolved with well disinfection and retesting (1 to 2 weeks). High nitrate levels or heavy metal contamination require treatment systems, which take longer and cost more. Your lender will require a second water test showing compliance. In rare cases, continuing difficulties can delay closing or, in extreme situations, kill the deal unless you accept the risk in writing.

Who pays for the well water test on a USDA loan?

Typically, the buyer pays for the water testing. Some purchase agreements shift this cost to the seller, especially in competitive markets. Ask your real estate agent about local custom. If treatment is needed, negotiate who covers those costs during your purchase negotiation. There's no single USDA rule on this - it's handled in your purchase contract.

Are private wells tested differently than municipal water supplies?

Yes. Municipal water supplies are constantly tested by the water authority and regulated by different rules. Private wells have no ongoing oversight - they test once for the loan, then it's your responsibility. This is why the USDA requires a water test before loan approval. You own the well and its quality entirely once you close on your home loan.

Key Takeaways for USDA Loan Well Water Testing

Getting your well water test requirements right is mandatory when pursuing a USDA loan. Commence by understanding that the USDA requires testing through a certified laboratory to test for bacterial contamination, nitrate levels, and other contaminants defined by your state. Plan to budget $150 to $400 for testing, plus potential treatment costs if problems occur.

Contact your local health authority early to confirm exact testing requirements for your county. Work with your lender to identify approved labs and keep all documentation organized. If your water test fails, don't despair - many problems are fixable. Plan for treatment time and a retest, then move forward to closing.

The USDA Rural Development website offers more information on USDA loan programs and rural property standards. Your state's health department website lists certified labs and specific water quality rules for your area. A knowledgeable loan officer familiar with USDA loans can guide you through every step and answer questions specific to your property.

Connect With Us

Please share – it really helps